YOUR BUSINESS AUTHORITY

Springfield, MO

YOUR BUSINESS AUTHORITY

Springfield, MO

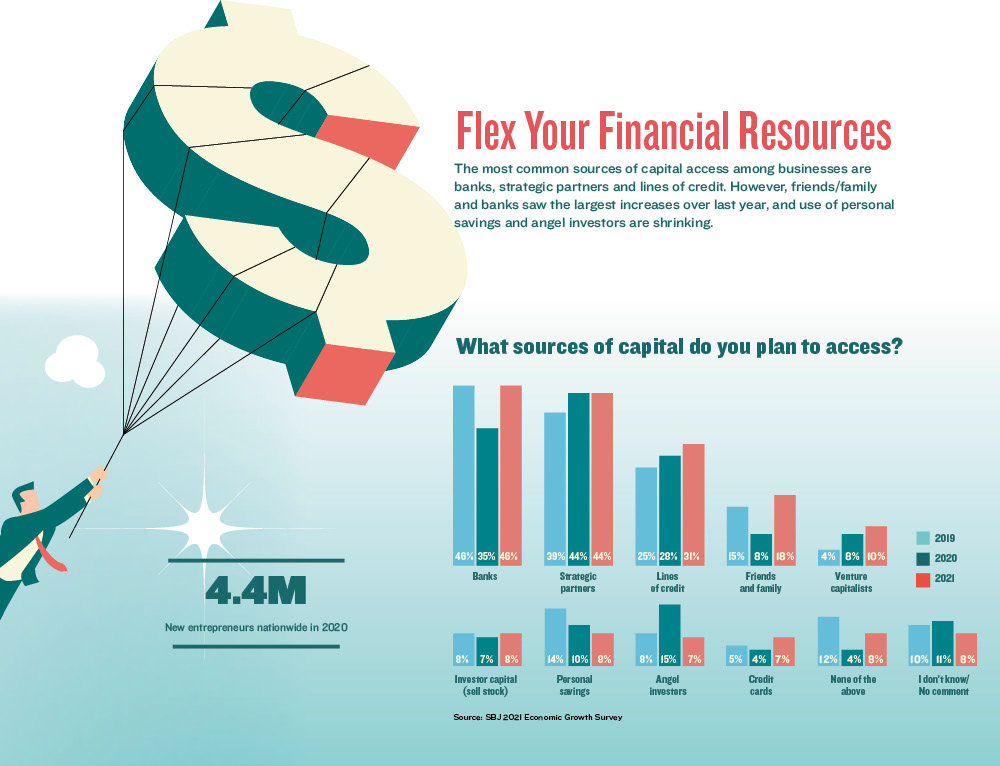

During the COVID-19 shutdown, many people got bored and turned to new hobbies, like learning yoga or making sourdough bread. But a whole lot of folks decided to become entrepreneurs – 4.4 million of them in 2020, according to the U.S. Census Bureau.

Starting a business requires capital, and that part of the puzzle may be trickier for people with a passion for a product or service but without a financial background.

Springfield Business Journal’s 2021 Economic Growth Survey reveals a year-over-year uptick in bank lending as a source of capital. When asked about the sources of capital business owners and leaders intended to draw on, 46% cited banks in 2021, up from 35% in 2020. A big increase also was recorded in the area of friends and family, with 18% of survey participants intending to access capital from those sources in 2021, versus 8% in 2020.

To Guy Colby Mace, managing partner at Baron Venture Capital LLC, the reason is obvious.

“It’s because of COVID,” he says. “People are sitting around reassessing, and if I’m going to start a business, guess who the easiest place to go is? It’s friends and family. That’s why there’s a spike.”

Mace has seen a shift recently, with other funders – hedge funds, private equity and some banks – stepping into venture capital turf. He says, as a result, he’s looking at funding projects he might not have considered before.

“VCs are just getting a lot of competition from traditional institutions because of the nature of the world we’re into right now,” he says.

SBJ’s annual survey shows a jump in interest in VC from respondents, with 10% intending to seek VC funding in 2021, compared with only 4% in 2019.

While it’s possible to get creative with capital, with means ranging from crowdfunding to foundation-based microloans, area bankers hope business owners, new and established, will keep in mind the resources they can find at their financial institutions.

“From a banking standpoint, we see things every day, so banks can be a great resource for small-business owners to navigate all things financially,” says Marcus Harmon, vice president and loan officer at Old Missouri Bank.

Additionally, friends and family don’t report to credit agencies, so there is no mechanism for strengthening credit through that type of funding, Harmon says.

“I’ve seen people borrow from family, and it can have a negative effect on family dynamics. That’s one of the potential pitfalls,” Harmon says. “There are cases where it’s worked.”

Harmon added that crowdfunding – raising capital through small amounts from a large number of people, usually via social media – also has its disadvantages, including fees and loss of equity.

“On that route, there are some fees that the platform you use is going to charge you,” he says. “You have to give up equity in a lot of cases.”

Doug Neff, chair and CEO for the southwest region for Commerce Bank, also sees value in businesses having a relationship with a bank.

“One of the advantages of working with a bank is typically you’re going to get to work with somebody who has a long history of helping business owners navigate challenges and opportunities,” he says.

Neff says capital is just one business need. Others include cash flow related to receiving payments and making payments, payroll processing needs and 401(k) offerings.

“Banks oftentimes have a lot of experience and can offer product sets to help the business owner,” he says.

According to Neff, having a banker on one’s side can also help to flatten the financial learning curve.

“Entrepreneurs are creative, and they have a passion for whatever they’re trying to create, but sometimes the emotion of that can be a block,” he says. “When you do work with a banker, you get a lot of financial expertise, and a lot of entrepreneurs and startups really need that.”

Still, not everyone goes the banking route. Some businesses, particularly those that rise from the home-based gig economy, grow in stages, using their own revenue as capital, also known as bootstrapping.

One entrepreneur who built her business from revenue is Amanda Layman, owner of Tigris Content Marketing, which offers business-to-business marketing campaigns. Layman started as a freelancer, working on a project-by-project basis. This year, Tigris is on track for $250,000 in revenue.

“The evolution from freelancing to running my agency was very slow-paced and organic,” she says, recalling that she went from writing all the time to handing off work to a stable of reliable subcontractors and hiring a project manager.

In the past two years, she has doubled Tigris’ business each year.

“I didn’t consider bank loans in the beginning for a couple of reasons,” she says. “One, I was terrified of getting into more debt, since I already had student loan debt and some old credit card debts that were haunting me. And two, I don’t think my credit would have been good enough to qualify anyway.”

But Layman thinks using her revenue as capital helped her business while teaching her some valuable lessons.

“It also helped to have so much of my own skin in the game,” she says.

The SBJ Economic Growth Survey found that on average, businesses expect 2021 revenue to increase about 4% over 2020, making bootstrapping an appealing source of capital.

For most businesses, capital sources are not an either-or proposition, and a range are used. Old Missouri and Commerce banks both participate in Small Business Administration programs, like the 7(a) loans for startups or SBA 504 commercial real estate financing. The U.S. Department of Agriculture also has loans, usually with a rural focus, and that’s another instrument available through banks.

“I come from a family of bankers, and I’ve seen banking relationships do all kinds of different things,” Harmon says. “For small-business owners, I feel like a banking relationship is just a major resource to navigate growing a business.”

Alair Springfield is first Missouri franchise for Canada-based company.